AI is fundamentally rewriting the rules of trade finance by enabling real-time risk assessment and dynamic discounting for mid-market suppliers. For analysts and associates, understanding these algorithmic shifts is the difference between managing a legacy ledger and architecting a modern liquidity engine.

The Death of the Manual Invoice

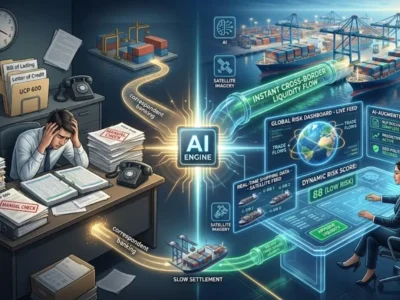

For decades, trade finance has been the “slowest” part of the bank. If you have spent any time in a mid-market lending or trade finance group, you know the pain: stacks of paper bills of lading, manual invoice matching, and a “waiting game” for liquidity that can stretch 60 to 90 days. It is a friction-heavy world where capital remains trapped in paper trails.

In our observation, the most significant shift over the last 18 months hasn’t just been “automation,” but the move toward predictive liquidity. Global Systemically Important Banks (G-SIBs) are no longer just processing transactions; they are using AI to predict when a supplier will need cash before they even ask for it. This is a game-changer for the Associate-level professional who is used to reactive relationship management.

The real-world impact is visible in how banks are integrating Natural Language Processing (NLP) to scan thousands of unstructured documents. Instead of an analyst spending six hours verifying a shipment of semi-conductors against an invoice, AI does it in seconds. This allows the bank to offer “Dynamic Discounting”—a process where the buyer pays the supplier early in exchange for a discount, with the bank facilitating the liquidity gap.

How G-SIBs are Automating Trust

Top-tier institutions like HSBC and JPMorgan are leading the charge by moving away from traditional credit scores toward “behavioral reliability” models. These models look at the historical performance of a supply chain rather than just the balance sheet of a single entity.

AI-Driven Fraud Detection in Trade

Trade finance is notoriously vulnerable to “double invoicing”—where a company seeks financing for the same shipment from two different banks. Historically, banks had no way of knowing this was happening until it was too late. Today, AI-powered platforms can identify patterns across global shipping databases to flag anomalies in real-time.

The Shift to Intelligent OCR

Optical Character Recognition (OCR) used to be a basic tool. However, the new generation of AI-integrated OCR doesn’t just “read” the text; it understands the context. It can tell the difference between a legitimate port authority stamp and a sophisticated forgery. This reduces the “Risk/Error Rate” significantly, allowing banks to lower the cost of capital for their clients.

Efficiency Analysis: Traditional vs. AI-Augmented

To understand why your senior MDs are obsessed with this, look at the delta between the old way and the new AI-augmented workflow.

| Factor | Traditional Trade Finance | AI-Augmented Trade Finance |

|---|---|---|

| Process Speed | 5 to 10 Business Days | Near Real-Time (Minutes) |

| Risk/Error Rate | 8% – 12% (Manual Entry & Fraud) | Less than 1% (Algorithmic Verification) |

| Operational Cost | High (Heavy Manual Labor) | Low (Scalable Software Tiers) |

| Liquidity Access | Fixed Term (30/60/90 days) | Dynamic (Instant Discounting) |

The Mechanics of Dynamic Discounting

As an analyst, you need to understand that “Dynamic Discounting” is the “killer app” of AI in banking. Here is how the workflow usually functions in a modern desk:

- Data Aggregation: The AI pulls data from the client’s ERP (Enterprise Resource Planning) system.

- Risk Scoring: The algorithm calculates the probability of the buyer defaulting based on current market volatility and shipping logs.

- The Offer: The system automatically offers the supplier an early payment at a sliding scale discount.

- Settlement: The bank captures the spread, the supplier gets immediate cash, and the buyer strengthens their supply chain.

This isn’t just a win for the bank; it’s a career-defining skill for you. If you can explain to a client how an AI-driven SCF (Supply Chain Finance) program can improve their DPO (Days Payable Outstanding) without hurting their suppliers, you are no longer just a “numbers person”—you are a strategic advisor.

Why Your Spreadsheet Skills are No Longer Enough

We often see junior bankers clinging to their Excel models like a life raft. While Excel is great for static data, it cannot handle the streaming data required for modern trade finance. The real value is moving toward “Data Interpretation.”

You don’t need to be a Python expert, but you do need to understand how to “prompt” or “query” the bank’s internal AI tools to find outliers in a portfolio. If you are still manually checking invoices, you are effectively working a job that is being phased out. The future of the Associate role is in supervising the AI’s output and handling the “edge cases”—the complex deals that the algorithm flags as too risky.

The Algoy Perspective

The real winner here will be the banks that successfully bridge the gap between their legacy mainframe data and these new AI layers. The biggest mistake firms are making is assuming that AI is a “plug-and-play” solution.

While AI is powerful, most banks still struggle with messy data silos that make implementation a nightmare. You will find that the “AI” at many banks is actually just a very complex set of IF/THEN statements because their underlying data is too disorganized for true machine learning.

The reality check is this: The banks that will dominate the next decade are not those with the best AI, but those with the cleanest data. If you want to future-proof your career, get involved in “Data Governance” projects now. It sounds boring, but it is the foundation upon which every successful AI strategy is built. If you can help your group clean its data, you become the most valuable person in the room when the AI tools eventually roll out.

Sources and Further Reading

- JPMorgan Newsroom: https://www.jpmorganchase.com/newsroom

- HSBC News and Media: https://www.hsbc.com/news-and-media